Rising farm costs could create fresh pressure across agricultural machinery supply chain

A widening gap between rising farm input costs and falling commodity prices is creating growing concern across UK agriculture, with analysts warning that a new “Cost of Farming Crisis” may be emerging.

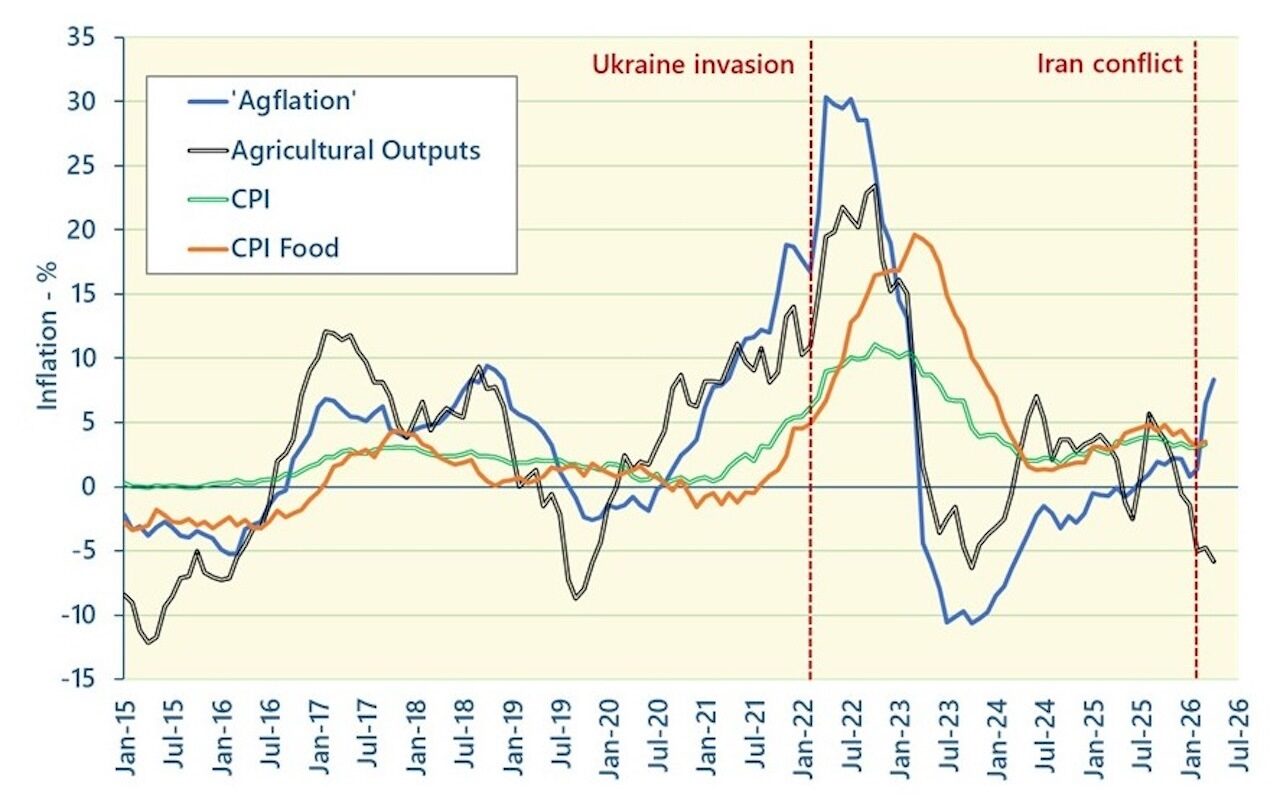

According to the latest estimates from Andersons Farm Business Consultants, agricultural input inflation — or “Agflation” — reached 8.4% annually in April 2026, significantly above UK CPI inflation at 3.3% and well ahead of the Bank of England’s 2% target.

At the same time, agricultural output prices have reportedly fallen by 5.8% year-on-year, placing additional pressure on already tight farm margins.

The latest cost increases are being driven largely by ongoing instability in the Middle East and concerns surrounding shipping through the Strait of Hormuz, a key route for global oil, gas and fertiliser movements. Around 30% of global urea supply passes through the region, pushing UK urea fertiliser prices to an estimated £650-700/t, while ammonium nitrate prices are also rising alongside gas markets.

Livestock sectors appear particularly exposed. Milk prices are currently around 25% lower than a year ago, pig prices have fallen by 12%, and beef values are also below 2025 levels.

For the agricultural machinery industry, the implications could become increasingly significant during the second half of 2026.

Higher fertiliser, fuel and electricity costs are likely to reduce farm cashflow and delay machinery purchasing decisions, particularly for discretionary capital investments. Dealers may see customers extending replacement cycles, prioritising repairsand refurbishment over new machine purchases, or increasing demand for used equipment and lower-cost ownership models.

Machinery manufacturers and suppliers are also likely to face further production cost inflation. Steel, energy, logistics and component costs remain sensitive to energy markets and global shipping disruption, while higher transport costs could continue to affect parts availability and delivery times.

At the same time, precision farming technologies capable of reducing input use may see stronger demand. Systems that improve fertiliser application accuracy, fuel efficiency, machine utilisation and labour productivity could become increasingly attractive as growers look to offset rising operating costs.

While cereal prices have improved in recent months, concerns over dry weather and potential yield reductions are creating further uncertainty ahead of the 2026 harvest and autumn drilling season.

Related news:

Oxford Farming Conference Question Time Highlights Priorities on Policy, Trade and Data